Banks leverage technology to meet customer demands. Disruption in retail banking continue to force traditional players to innovate and respond to the market. With high pressure to boost revenues and reduce costs, delivering valuable customer experiences are paramount to keeping up with new banking technologies. .jpg?width=622&name=1200x627%20(45).jpg "banking technologies") These transitions are monumental as banks invest in new technologies such as blockchain, Artificial Intelligence, robots, mobile payments, and Digital ID to drive efficiency, convenience, and security. Early adopters will stay ahead to compete with their FinTech and digital-only counterparts.

These transitions are monumental as banks invest in new technologies such as blockchain, Artificial Intelligence, robots, mobile payments, and Digital ID to drive efficiency, convenience, and security. Early adopters will stay ahead to compete with their FinTech and digital-only counterparts.

This shift means banks need to abide by regulatory safeguards, keep their customers happy, increased transaction transparency, while maintaining security and trust. This delicate balance has created a marketplace for both internal and external new technological solutions. Here are the 7 latest trends in banking.

This shift means banks need to abide by regulatory safeguards, keep their customers happy, increased transaction transparency, while maintaining security and trust. This delicate balance has created a marketplace for both internal and external new technological solutions. Here are the 7 latest trends in banking.

1. Banks are investing in digital transformation

For CIOs and other banking executives, digitization is still a top priority to maintain a competitive position and reduce the risk of a being replaced by more efficient and credible alternative.

In spite of the widespread knowledge of bank technologies, the transition is taking time. Technologies are ready, but are still in the early adopter phase. First movers like HSBC and Barclays still see a great need to educate customers. The transition for even the most innovative leaders will require training bank personnel to introduce current and new client base to technological advances. HSBC study shows that customers expect banks to:

-

Providing customers support if technology goes wrong (74%)

-

Advising customers on how the new technology can meet their needs (65%)

-

Giving advice and information online (57%)

2. Digital ID

Digital identification goes beyond authentication. Advanced biometrics-based solutions like fingerprints, iris, vein, face, and voice recognition can help banks service customers and mitigate fradulent behavior.

At the same time customers expect seamless service across channels without going through repetitive verification.

In 2016 HSBC launched voice recognition and touch security services in the UK to over 15 million banking customers in a big leap towards the introduction of biometric banking. This year along with Barclay's HSBC is testing digital ID for cross-border banking.

3. RPA and AI from Adoption to Increased Efficiency

From 2015-2018 banks pull sources to adopt robotic process automation (RPA) and artificial intelligence (AI). Accenture estimates that within 2015-2018 a total of $19.6 billion in professional services robots will be sold. Beyond 2018 the main driver will be cost optimization and operational efficiency.

RPA offers automation of repetitve and mundane tasks. Banks that leverage the power of AI and the surging popularity of cognitive technologies on top of RPA technology will increase efficiencies and lead digital transformation.

For banking specifically, the adoption of artificial intelligence brings a host of new benefits and cost-efficiency. In fact, 86% of bank executives agree that the widespread use of AI provides for a competitive advantage beyond cost. Those same executives said they plan on using machine learning to drive automation in customer service and IT.

To reap the full advantages of maching learning and automation first-line, middle-level and executive- level managers need effective and timely training to increase skills set in order support full implementation. 57% said that their current skills are lacking and have an incomplete understanding is required to thrive with intelligent machines.

There will be a learning curve and integration time for banks to see the expected transformation. Banks should aim to create a culture that is symbiotic and accepting of advanced machines and banking technology.

4. Mobile Technology and Applications Will Replace Old Processes

At the very minimum, most banks offer a mobile banking app that can process transactions and replace traditional paper balances. A 2016 report by BBA found that in 2015, UK banks processed 347 million payments via mobile – a 54% increase from the year before.

In the US, there are over 111 million mobile banking users. This means that one in three US citizens currently use mobile banking. The popularity of mobile first solutions is only on the rise as security improves and people feel safer using mobile banking features.

Figure 1 Source: Statista

Almost 70% of the Gen Z generation use mobile banking apps daily, with 68% wanting instant P2P payments. While being mobile-first, this generation also uses other channels more than other generations.

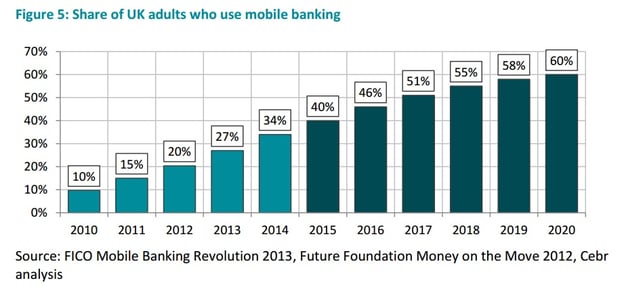

Currently, just over a third (34 percent) of U.K. adults are estimated to be banking on their mobile. With the increasingly widespread ownership of smartphones and a growing appetite amongst UK adults to access their finances on-the-go, this figure is expected to almost double to 60 percent by 2020. This projected increase of 14.8 million more mobile banking users over the next half-decade represents a significant opportunity for challenger banks to bring their innovative business models to the market and for existing banks to add digital services to cater to this future majority.

Additionally, banks are looking externally at mobile application developers to streamline their training, onboarding, and compliance efforts. Mobile applications offer customized and scalable solutions that are modern, cost-effective, and could be the future of learning and training.

5. Banks Will Focus and Invest Heavily in Corporate Innovation

As banking becomes more digitalized, banks are recruiting and building tech teams, and in some cases full companies, under their global operations. To compete with leading tech giants, banks are now trying to build out products and solutions within financial technology (fin-tech), blockchain, cloud services, and mobile solutions.

Barclays, Wells Fargo, BNP Paribas, and a handful of other large global banks have created incubators that invest and build new ventures, focused mostly on disruptive fin-tech startups that directly solve major pain points within banking. Companies build these programs to be at the forefront of banking technology and part of the tech ecosystem. If they can’t build or fund a venture, they can utilize this innovative network to be early adopters.

6. Digital Safety and Trust Will No Longer Be a Major Hurdle

Figure 2 Source: Accenture

As with any new technology dealing with personal finances, consumer banks experienced an early backlash to mobile and online banking. A 2015 survey on Statista showed that 72% of people currently not using mobile banking cited security concerns as one of the reasons why. Fast forward one short year later and third-party P2P payment processors, such as Venmo and Paypal, have become more prominent than bank transfers.

In 2016, Venmo processed over $20 billion in payments through its mobile only application. This implies that people are not only becoming more assured by linking their bank information to payment processors, many do so with third-party apps that offer limited user protection.

For banks, trust and user protection rank as a top priority, with 84% of bank executives citing trust as the cornerstone of the digital economy in banking. By using a combination of cutting-edge banking technology for data protection, communication and ethics, and risk management, banks are starting to convert more and more customers in the digital economy.

7. Blockchain Will Combine All of the Above to Rise in Prominence

Blockchain technology is still a hurdle as customers need to educated on its benefits. It promises to reinvent digital security and trust by chaining together data and transactions within a distributed database that can’t be modified. In layman’s terms, this means that information can be shared but not changed. Blockchain's reliable track record could solve many compliance and security issues currently facing banks.

Also, Blockchain is completely transparent and can’t be corrupted. While still in its infancy, blockchain technology has reclaimed popularity after its initial exposure during the early bitcoin days. Banks are currently scrambling to find a way to incorporate blockchain technology. The excess of sensitive information that banks deal with makes it difficult toincorporate.

Preparing banking employees in times of digital transformation

More than 60% of banks believe that success hinges on new skills. Expertise in the ability to market through multiple channels, to integrate IT across them, to develop smartphone apps, and to convert digital transactions to sales. By contrast a majority of them have less than 10 people dedicated to mobile. To stay ahead, banks will need to retrain and upskill current staff or hire for missing skills.

Manual processes of KYC and AML take a heavy toll on banks in terms of human and financial resources thus there is need of more automation to enhance efficiency and reduce costs. But until banks are fully transformed, employees will need to support the transition process for banking customers to adopt the new technologies.

How are financial institutions onboarding employees in a time of increasingly complex compliance and regulation?

How are financial institutions onboarding employees in a time of increasingly complex compliance and regulation?

What's technology's impact and how are companies already using it?

- State of the industry's technology

- Banks & mobile apps: can they benefit?

- Onboarding and innovation in banking

- Onboarding implementations

- 10 facts on retention, training, and talent sourcing

- Exclusive TLDR summary

.jpg)

.jpg)

.jpg)